AI Agents Are Breaking SaaS

How AI Agents are changing Saas Pricing Models!

How to price AI Agents?

For about twenty years, the SaaS pricing model worked because one assumption held. More employees meant more software licenses. Hire 50 salespeople, buy 50 CRM seats. Hire 20 accountants, pay 20 seat fees. Hire a customer support team, pay per agent. Software valuations, go-to-market strategies, and entire revenue models were built on that relationship.

That equation is now wrong.

AI agents don’t need seats. They don’t log in. They don’t accumulate usage history in a user profile. They execute work, sometimes thousands of tasks at a time, without showing up in any admin dashboard. And when one AI agent can do the work that used to require ten, twenty, or fifty human users, the per-seat model doesn’t just compress. It breaks.

This isn’t a theoretical shift anymore. The data has arrived, and it’s striking. Per-seat pricing dropped from 21 percent to 15 percent of SaaS companies in just twelve months. Gartner predicts at least 40 percent of enterprise SaaS spend will shift to usage-, agent-, or outcome-based pricing by 2030. Bloomberg estimates that subscription-based pricing could decline from 60 percent of software pricing models to 30 percent over the next decade, while outcome-based pricing could climb from 10 percent to 60 percent.

What’s actually happening underneath these numbers is something I think deserves more careful attention than it’s getting. So let me try to unpack it.

Why per-seat pricing was always measuring the wrong thing

Here’s the part people don’t say out loud. Per-seat pricing was never about value. It was about proximity to value.

In the early SaaS era, the number of human users was a reasonable stand-in for value delivered. More users meant more workflows supported, more data created, more lock-in built up over time. But vendors couldn’t actually measure outcomes. Did the CRM close more deals? Did the project management tool ship projects faster? Nobody really knew. So they measured access instead. Seats. Licenses. Logins.

This worked for decades, partly because everyone was used to it and partly because the alternative was too hard. There was no reliable way to attribute outcomes to specific software, so vendors and buyers settled on a shared fiction. Pay for access, and we’ll all agree that more access equals more value.

AI agents have made that fiction visible. When the agent is doing the actual work, not just supporting a human who does it, the unit of value becomes the work itself. The outcome. The resolved ticket, the processed invoice, the qualified lead. And once you can measure outcomes directly, charging for access starts to look like what it always was. A proxy that no longer makes sense.

What’s replacing it

Three pricing models are emerging as alternatives, and the most successful SaaS companies are usually combining them rather than choosing one.

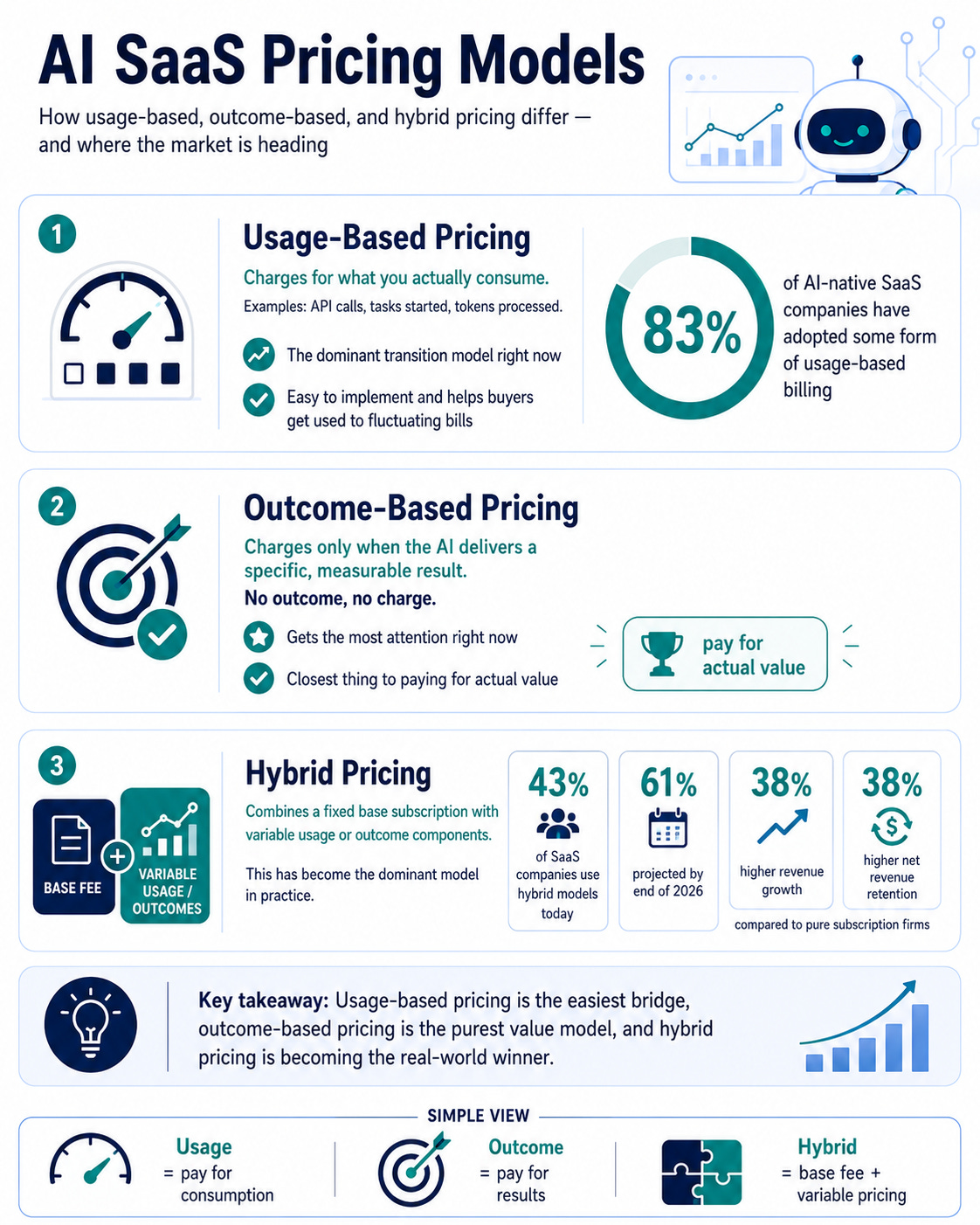

Usage-based pricing charges for what you actually consume. API calls, tasks started, tokens processed. This is the dominant transition model right now, partly because it’s the easiest to implement and partly because it acclimates buyers to fluctuating bills before they’re ready to commit to outcome pricing. Around 83 percent of AI-native SaaS companies have already adopted some form of usage-based billing.

Outcome-based pricing charges only when the AI delivers a specific, measurable result. No outcome, no charge. This is the model getting the most attention, and for good reason. It’s the closest thing to “pay for actual value” that the software industry has ever managed.

Hybrid pricing combines a fixed base subscription with variable usage or outcome components. This has become the dominant model in practice. Around 43 percent of SaaS companies now use hybrid models, projected to hit 61 percent by end of 2026. Companies using hybrid pricing report 38 percent higher revenue growth and 38 percent higher net revenue retention compared to pure subscription firms.

The interesting question isn’t which model wins. It’s which model fits which type of work.

How this looks in accounting

Bookkeeping is one of the cleanest examples of how AI agents are rewriting SaaS economics, because the unit of work is so easy to define.

Traditionally, accounting software charged per user. You bought seats for your bookkeepers, accountants, controllers. The platform supported them while they did the work. QuickBooks and Xero built billion-dollar businesses on this model.

Now look at what’s happening. Pilot announced in February 2026 what it calls the world’s first fully autonomous AI Accountant for small businesses, running the entire bookkeeping process from onboarding through monthly close with zero human intervention. Vic.ai automates accounts payable workflows by ingesting hundreds of invoices and categorizing them without manual uploads. Docyt connects to bank feeds and over 30 POS systems, with agents that handle document extraction through financial variance analysis. Receiptor monitors email inboxes in real time, extracts data across languages and currencies, and routes clean data to QuickBooks or Xero.

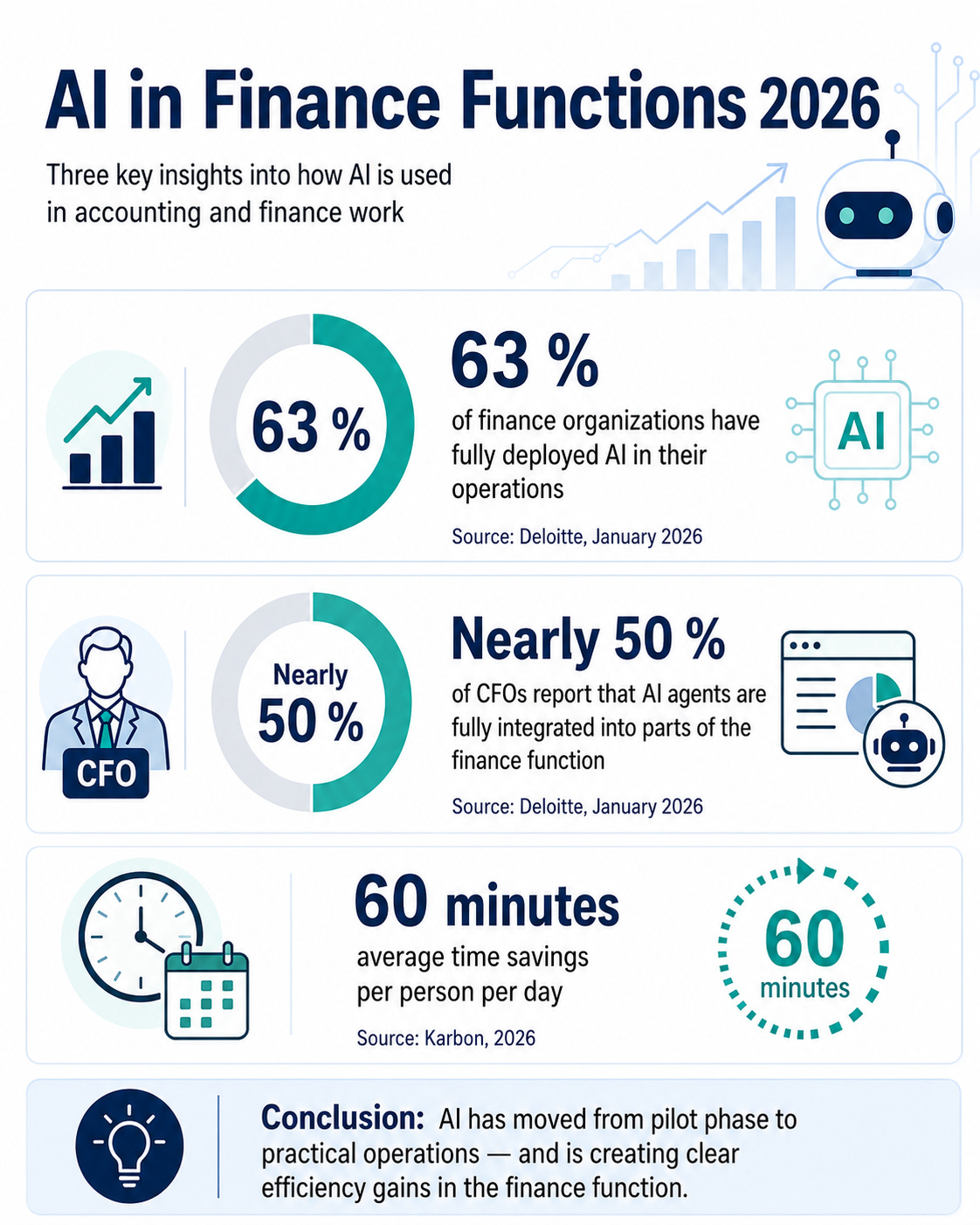

The fundamental shift is that you’re no longer paying for software that helps a human accountant. You’re paying for the work the accountant used to do. A January 2026 Deloitte study found that 63 percent of finance organizations have fully deployed AI in their operations, and nearly half of CFOs report having fully integrated AI agents into parts of the finance function. Average time savings, according to Karbon’s 2026 data, sits at 60 minutes per person per day. Once those minutes compound across a firm, the headcount that justified per-seat licenses starts to look very different.

The pricing implication is obvious in retrospect. If one AI agent processes the invoices that used to require five clerks, the vendor that still charges per seat is leaving most of the value on the table. The vendor that charges per invoice processed captures it. That’s why the most aggressive AI-native accounting platforms are moving toward outcome-based or hybrid models, and why the incumbents are scrambling to follow.

How this looks in customer support

Customer support is where outcome-based pricing has gone furthest, fastest. The unit of work is so easy to define (a resolved ticket) that the entire industry has converged on the same metric within eighteen months.

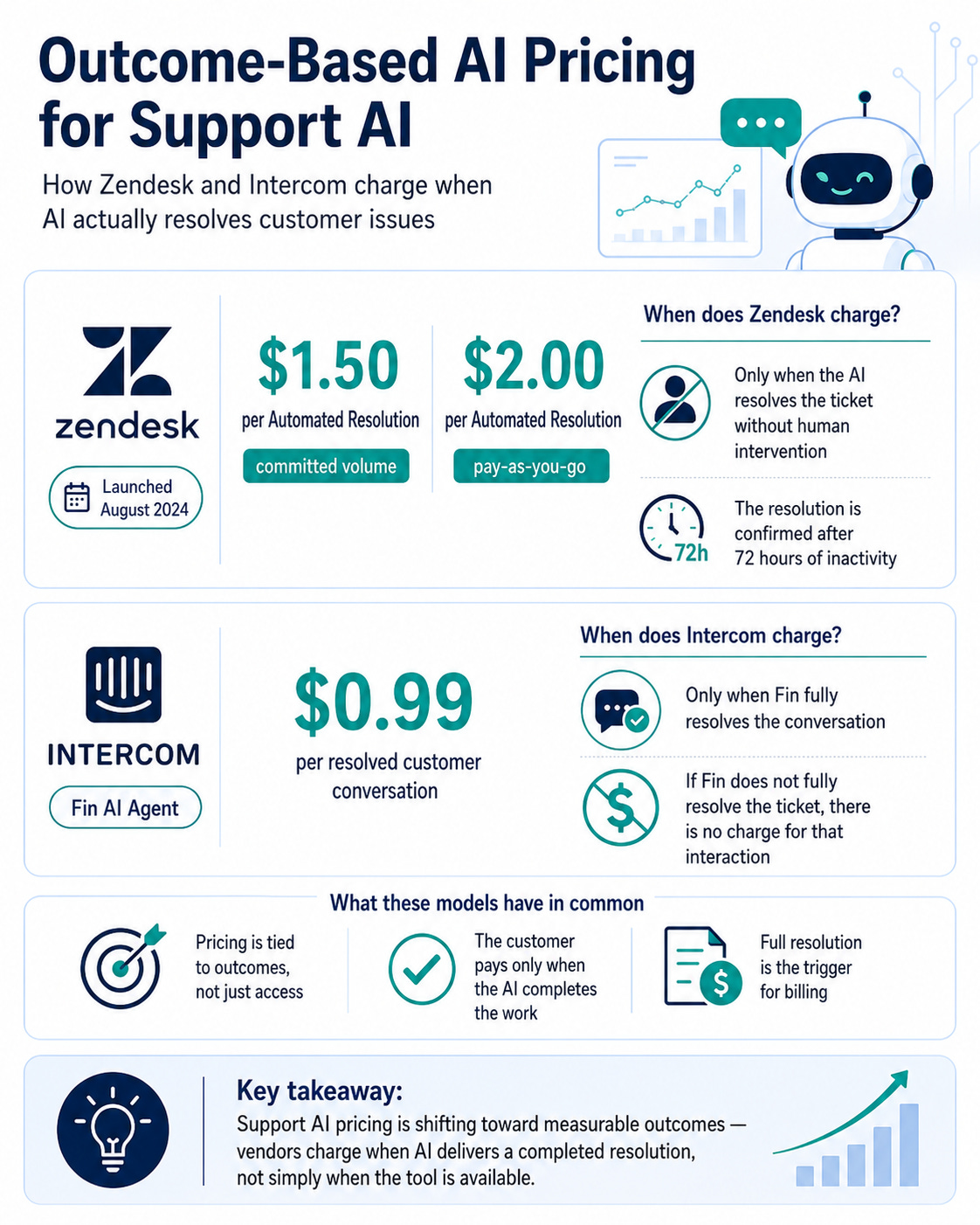

Zendesk launched outcome-based pricing in August 2024, billing at $1.50 per Automated Resolution on committed volume and $2.00 pay-as-you-go. A resolution counts only if the AI handles the ticket without human intervention, confirmed after 72 hours of inactivity. Intercom charges $0.99 per resolved customer conversation through its Fin AI Agent. If Fin doesn’t fully resolve the ticket, the customer doesn’t pay for that interaction. HubSpot dropped its Customer Agent pricing to $0.50 per resolved conversation in April 2026. Sierra built its entire business model around outcome-based pricing for customer experience AI agents.

What’s worth noticing here is the alignment. The vendor only gets paid when the AI actually solves the customer’s problem. The buyer only pays for outcomes that landed. The incentives are pointing in the same direction in a way that per-seat pricing never quite managed.

The catch, and there’s always a catch, is definition. What counts as “resolved” varies between vendors, and the contract terms around it can be gamed if not specified carefully. The buyers winning here are the ones who treat the Outcome Measurement Agreement as a prerequisite, not a procurement detail.

How this looks in CRM

CRM is the interesting case because Salesforce, the company that defined per-seat SaaS, is in the middle of openly restructuring its business model.

Salesforce introduced the Agentforce Enterprise License Agreement (AELA), which gives enterprise customers unlimited use of Agentforce, Data 360, and MuleSoft for a fixed fee on two- or three-year terms. This is the most visible large-incumbent template for how enterprise AI pricing transitions away from per-seat metered billing. Underneath the surface, Salesforce is also experimenting with consumption-based Agentforce credits for organizations not ready for the all-in commitment.

The strategic logic is clear. If Salesforce continued charging per sales rep while AI agents reduced the number of reps needed, revenue would collapse. So they’re repositioning the value unit from “access to the platform” to “access to the agent capacity that does the work the platform was always meant to deliver.” HubSpot has moved in a similar direction with its Customer Agent. ServiceNow has restructured pricing around workflow automation outcomes rather than seat counts.

This is what it looks like when an incumbent reads the wind correctly. The companies that started the transition early are now ahead of competitors still defending per-seat models. The market is punishing the laggards. The February 2026 “Black Tuesday for Software” sell-off, when investors collectively realized that seat-based business models were structurally exposed to AI, took meaningful market cap out of several well-known names.

What this means for tech leaders

Three implications worth taking seriously this quarter, whether you’re a buyer or a builder.

1. Your existing SaaS contracts probably mis-price what you actually use. If your organization has deployed AI assistants or agents inside your existing tools, you’re likely paying for headcount that no longer reflects your actual usage. Renewal negotiations are a real opportunity here. Push for hybrid pricing with a hard consumption ceiling when AI adoption is still early in your organization. Move to usage-based when patterns are stable. Only commit to outcome-based when you have the instrumentation to verify outcomes independently. The transition window for these conversations is 2025 to 2026. After that, the vendors will have set the terms, and you’ll be inheriting them rather than shaping them.

2. If you’re building software, the unit of value question is now urgent. The companies winning in the new SaaS economy are the ones that have clearly defined what “an outcome” looks like in their domain and built the instrumentation to measure it reliably. The companies losing are the ones still selling seats for products that increasingly don’t need users. Three tests worth applying: Can you define an outcome that’s technically verifiable? Can you cleanly attribute that outcome to your AI? Will your customer agree on what counts as success before signing? If you can answer yes to all three, outcome pricing is worth exploring seriously. If any answer is “maybe,” stick with usage or hybrid until you can.

3. The bigger strategic shift is that software is moving onto labor budgets. This is the part I think most leaders haven’t fully absorbed. When you charge per seat, you’re competing for IT budget. When you charge per outcome, you’re competing for labor budget. The labor budget is roughly ten times larger. The companies that successfully reposition their products from “software you buy” to “work you hire” are tapping into a fundamentally different pool of money. That’s why AI-native vendors are pricing more aggressively than their per-seat predecessors, and why investors are valuing them on different multiples.

The honest part

I don’t want to oversell this transition. There are real problems with outcome-based pricing that the industry hasn’t solved yet.

Attribution is hard. When an AI agent works alongside a human, who gets credit for the outcome? When multiple tools are involved in a workflow, how do you split the value? When the customer changes their definition of success mid-contract, what happens to revenue recognition? These aren’t theoretical questions. They’re the kind of accounting problems that make CFOs nervous and slow down enterprise procurement cycles.

The unit economics also remain genuinely uncertain. AI agents have meaningful inference costs that don’t exist in traditional SaaS. Every task an agent performs costs real compute, real API calls, real tokens. If your outcome price is $0.50 and your inference cost is $0.30, your gross margins look very different than a 90-percent-margin SaaS product. Some of the AI-native companies pricing aggressively today are doing so partly on the bet that inference costs will keep falling. They probably will. But “probably” is a different word than “definitely.”

And the transition itself is going to be uneven. Not every workflow can be cleanly outcome-priced. Knowledge work that requires judgment, creativity, or relationships will stay on hybrid or per-seat models for a long time. The clean wins are in high-volume, measurable, repeatable work. Customer support. Back-office finance. Code generation. Lead qualification. The rest will be messier.

The bigger picture

Here’s what I think is actually happening.

For two decades, SaaS pricing was about access. Buy a seat, get a license, use the tool. The tool was the product, and the human user was the unit of measurement. AI agents have inverted that. The agent is now the product, the work is now the unit of measurement, and the human is increasingly the supervisor rather than the operator.

When the unit of measurement changes, everything downstream of it changes too. Pricing changes. Sales motions change. Contract structures change. Procurement processes change. The competitive landscape changes, because the moats that protected incumbents in the seat-based world (entrenched user bases, switching costs, training investments) matter less when the user disappears.

The companies that internalize this early will spend 2026 and 2027 building products and contracts that match the new reality. The ones that don’t will spend those years watching their renewals erode and their gross margins compress, wondering why the old playbook stopped working.

The SaaS business model isn’t dying. It’s just changing what it measures, what it charges for, and who it sells to.

The question for every tech leader right now is whether you’re shaping that change or inheriting it.

This is a great look at the next major headache for IT and finance teams. Managing 'shadow AI' and agentic tools that don't require user logins makes classic SaaS management obsolete. I've been seeing Najar pop up a lot in discussions around this exact problem lately, they seem to be one of the few platforms adjusting to track procurement and spend in an agent-heavy environment rather than just auditing standard user seats. Thanks for sharing this perspective!